Wow

Can you say bubble?

Can you say Virus? LOL

Weird, every time, this is what I got coming to this Thread. Only this Thread.

Wow

Can you say bubble?

Yeah Weird, I saw this yesterday too, what is also weird is it only pops up on page 109 of this thread...so it must be something on that page, some preview site...not thinking an X post...Click on 'See Details"

Im running two different AV systems and a firewall appliance with IPS and I'm not seeing it

You're likely seeing something like this

PR_CONNECT_RESET_ERROR

Its because the website itself isnt live. I have no idea the owner, but trust that X has way better security than you or I

") What's he doing, lol

What's he doing, lol

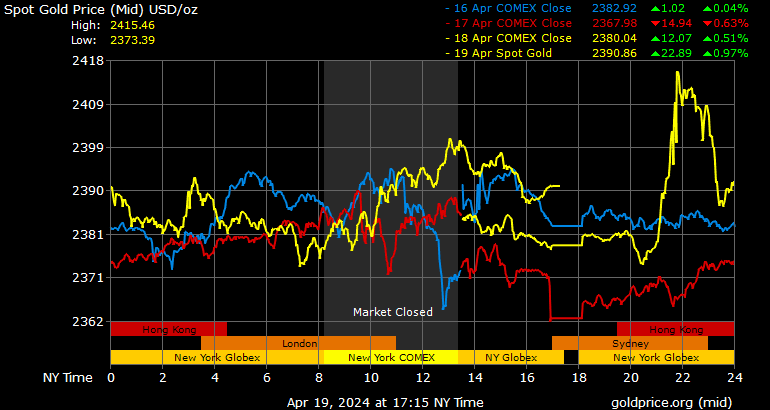

Gold took a nosedive today didn't it?

Gold took a nosedive today didn't it?

Wow

Can you say bubble?

Except you copied the current bracket chart. The 2026 chart is further down on the page. I got caught by the same thing, the headline says "new" brackets then the first thing they show is the old/current brackets.The new tax brackets are out...

good catch man--- I added the 2026 chart to that reply-- interesting comparison.Except you copied the current bracket chart. The 2026 chart is further down on the page. I got caught by the same thing, the headline says "new" brackets then the first thing they show is the old/current brackets.

Money withdrawn from a traditional IRA is taxed as ordinary income, regardless of what it might be (capital gain, for instance). The thing to watch out for, if getting social security and under the maximum social security taxation of 85%, AND in the 12% marginal tax bracket, is whatever you withdraw will increase the social security taxation rate, with the net effect being 22% federal tax on what you withdraw.